The impacts of COVID-19 on electricity demand in the National Electricity Market (NEM) are relatively well documented by various commentators, including recently by the Australian Energy Market Operator (AEMO)[1] and the Australian Energy Market Commission (AEMC)[2]. In brief, observed reductions in electricity demand in the NEM due to COVID-19 appear to be less than 10% as compared with reductions of up to ~30% observed in Italy and other countries with tighter restrictions. The obvious follow-on question which is less well documented is ‘has there been a corresponding impact on East Coast gas demand due to COVID-19’?

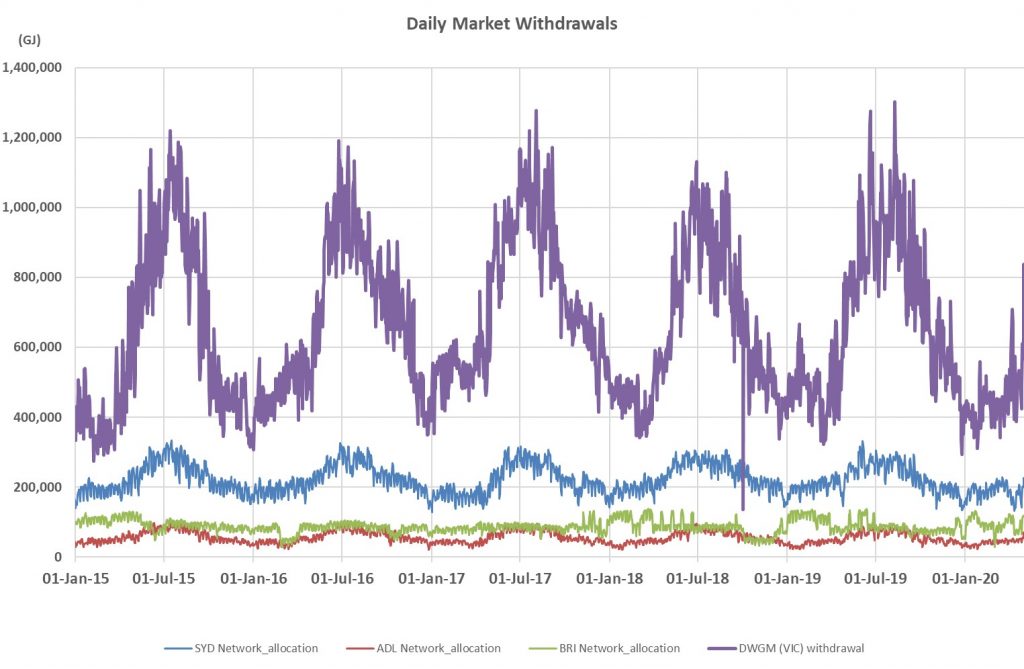

While not completely representative of total domestic gas demand, gas that flows through the Victorian Declared Wholesale Gas Market (DWGM) and the Short-Term Trading Markets (STTM) of Adelaide, Brisbane and Sydney represent a large proportion of East Coast domestic demand. There of course remain some industrial users, gas powered generators and regional centres (of residential and commercial demand) that sit outside these markets. Nonetheless, the three STTM markets and the Victorian DWGM have historically totalled on a combined basis around 1,700 TJ/d at winter peak, down to lows of around 750 TJ/d during summer (Figure 1).

Figure 1: gas flows for various East Coast gas markets from 01-Jan-2015 to 30-Apr-2020 (data source: AEMO)

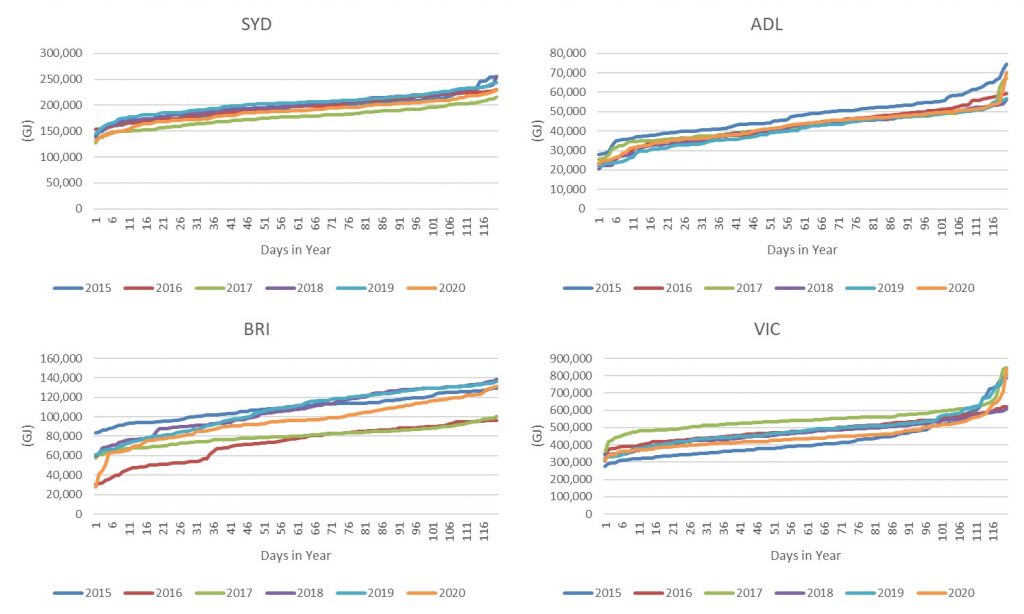

Any potential impact of COVID-19 on East Coast gas demand to date would have been over the first four months of the year from January to April 2020. Anecdotally from Figure 1 there appears to be little difference between the last few months of gas flows through these four markets compared with recent prior years. However, Figure 2 shows a more insightful comparison of minimum to maximum demand days over the period January to April for each of the calendar years 2015 to 2020 across the four markets. From this one can clearly observe that domestic gas demand over the first ~120 days of 2020 appears to fall within recent historic norms.

Figure 2: comparison of minimum to maximum peak days for January to April (data source: AEMO)

Does this mean there is no domestic gas demand impact due to COVID-19?

Not necessarily. While residential and commercial demand is likely to revert to near normal trends once COVID-19 restrictions are eased, gas power generators and industrial users may experience longer lasting impacts.

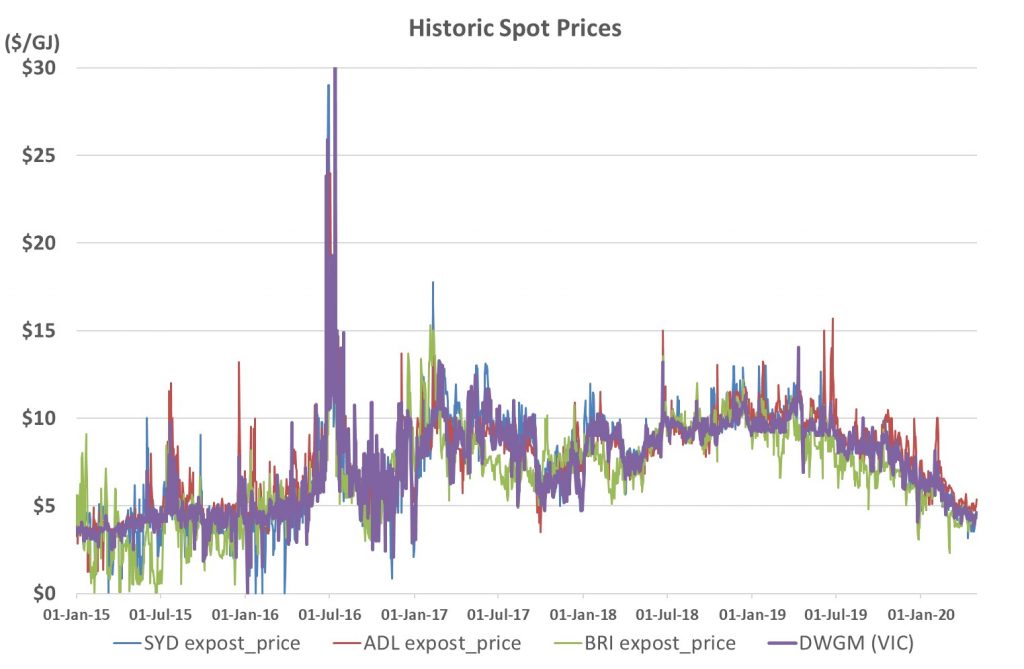

Falling global oil and LNG prices has also resulted in supply side downward pressure on domestic gas prices, which in turn makes gas powered generation more price competitive in the NEM than it has been for some time (refer also [2] for more explanation). Lower gas prices may therefore increase the demand for gas powered generation, albeit for the limited number of generators that are able to trade the spark-spread between gas and electricity prices within their energy portfolios or opportunistically on the spot markets. Figure 3 illustrates the spot gas market prices over time since 2015, with a clear downward trend in spot gas market prices since Q2 2019, resulting in current observed prices averaging below $5/GJ for the month of April across all four markets. While there may be some direct impact on gas prices due to COVID-19, spot gas market prices have clearly been falling since well prior to January 2020.

Figure 3: spot market prices from 01-Jan-2015 to 30-Apr-2020 (data source: AEMO)

A number of industrial users of gas (including those not located within the networks of the STTM or the DWGM) may be exposed to export markets, where demand for their products are suppressed due to COVID-19 (e.g. in Europe, Asia and the USA). These industrial users will have reduced demand until their primary international export markets recover from the impacts of COVID-19. Conversely, some commentators have sighted that COVID-19 has highlighted flaws in global supply chains models, which present an opportunity for Australian manufacturing to fill gaps both in the short-term and longer term create a renascence of local manufacturing. If such a manufacturing renascence is realised in the coming years, it would potentially increase demand for domestic gas supply (subject to prevailing gas prices).

Has East Coast LNG production declined given falling LNG prices?

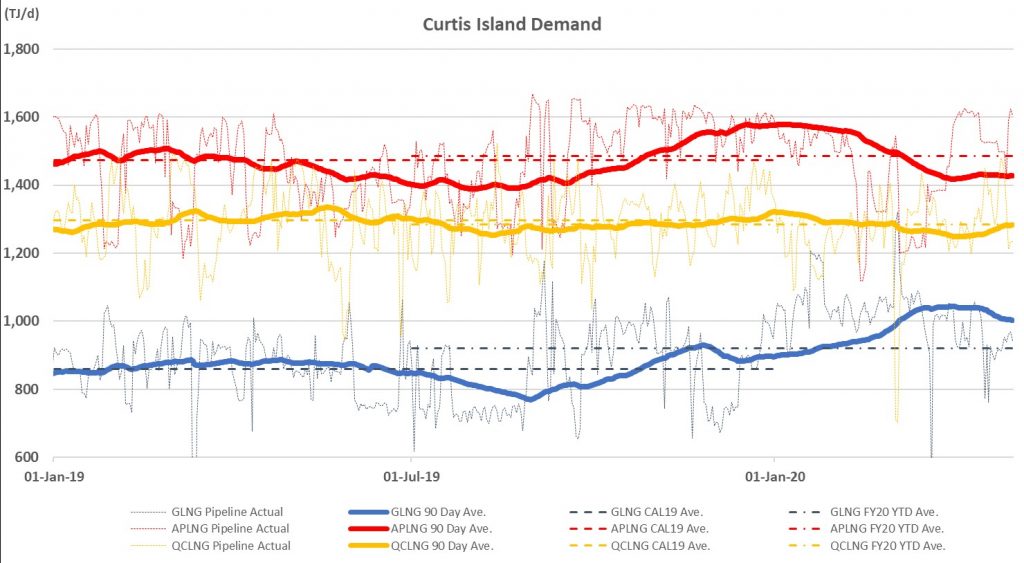

Not yet at least. In fact, LNG export production in aggregate across the three projects has increased since Q2 2019, with GLNG making a noticeable step-up in production since about when the COVID-19 pandemic began in January 2020 (Figure 4).

Figure 4: East Coast LNG export pipeline flows (data source: AEMO)

The recent uptick in GLNG production may correspond with lower domestic gas prices, especially if GLNG can purchase domestic gas at prices below upstream production costs that still provide for an export sales margin in the lower LNG price environment. Nonetheless, the downward price pressure since COVID-19 does not appear to be due to the LNG projects diverting supply from LNG cargoes into the domestic market, but is rather from greater domestic supply overall from the LNG projects in combination with new domestically focused supply projects (e.g. Cooper Energy’s Sole project).

About the author

Nicholas Mumford is Principal Consultant & Director at Mumford Commercial Consulting (www.mumfordcommercial.com.au), specialising in providing commercial advice in the Energy and Resources sectors.

[1] https://aemo.com.au/news/latest-covid19-demand-impact-summary

[2] https://www.aemc.gov.au/news-centre/economists-corner/whats-happening-wholesale-prices